By Etienne Lepers

Contemporary political analysis, though firmly focused on the yet to be created AIIB, should be equally as focused on the poorly covered Chinese bilateral lending relationships that already exist.

Contemporary political analysis, though firmly focused on the yet to be created AIIB, should be equally as focused on the poorly covered Chinese bilateral lending relationships that already exist.

China’s role in the global financial system has recently caught the media’s attention more than usual, as Beijing’s financial aspirations create significant diplomatic tensions among Western countries.

Specifically, the UK and other major European countries, against U.S. wishes, flocked to join the Chinese-led Asian Infrastructure Investment Bank (AIIB). The mainstream media focus on the discord among Western nations, however, should not cause observers to overlook key facts. It is important to note that China has already assumed, on a bilateral basis, both the roles of worldwide development lender, and of lender of last resort to countries in crisis.

During recent AIIB news coverage, China came to rescue Brazilian oil giant Petrobras with a $3.5 billion loan deal, and promised Pakistan $60 billion in massive infrastructure projects. These are just two examples of China’s longstanding and multifaceted lending actions.

The immediate political focus should not be on the yet-vague AIIB, whose precise features and role is still to be defined, but rather on the political dynamics of China’s bilateral relations with long-term loan recipients.

China And Its Numerous Friends

The problem with analysing Chinese lending is that Chinese banks rarely disclose information regarding their financing activities, thus preventing any systematic research effort or detailed media coverage.

Still some scholars, like Deborah Brautigam of Johns Hopkins and Kevin Gallagher of Boston University, have provided estimations: between 2003 and 2011, China lent $53 billion to Africa and $80 billion to Latin America, more than half of which were commodity-backed.

Venezuela has been the largest loan recipient, with 16 loans totalling $56 billion since 2005. Major lending ties have also been developed beyond Latin America and Africa: Ukraine, Sri Lanka and Myanmar have also become very reliant on Chinese loans for their infrastructure financing.

Alongside its role as development bank, China has also occassionally assumed the role of short term liquidity provider for countries in crisis, making the country a true lender of last resort. For instance, the Venezuelan government would already have defaulted if China had not come to the rescue. Indeed, investors have gauged the probability of a Venezuelan default at 90%.

Chinese loans originally allocated as long term funds for oil infrastructure development have been allowed to serve as foreign exchange reserves. The same story goes for Argentina, where Chinese cash was used to replenish its forex reserves.

As for Russia, when the ruble collapsed this year, China also offered a line of credit. Beijing’s actions were part of currency swap deals allowing these countries to exchange their falling local currency against the yuan.

What Motivations?

Beijing’s most obvious motivation is the promotion of China’s economic interests. Loans are part of China’s strategy to secure resources, especially oil and food. The fact that 55% of its loans are commodity-backed is evidence for this.

China also has geopolitical objectives, for in doing business with countries that have been abandoned by Western financial organs, China gains significant influence. With access to Western financial markets either impossible for defaulted countries (Argentina), or politically difficult for pariah states (Russia), Chinese loans give Beijing an important foothold. Unsurprisingly, China’s partners are mostly countries that clearly do not belong to Washington’s circle of friends.

Regardless of who the partner is, it is a fact that China is searching to diversify its investments away from US Treasury Bills (US T), which have appeared more risky than previously thought. The proliferation of lending in infrastructure projects can be seen as a way to find higher return than the low-yield US T bills.

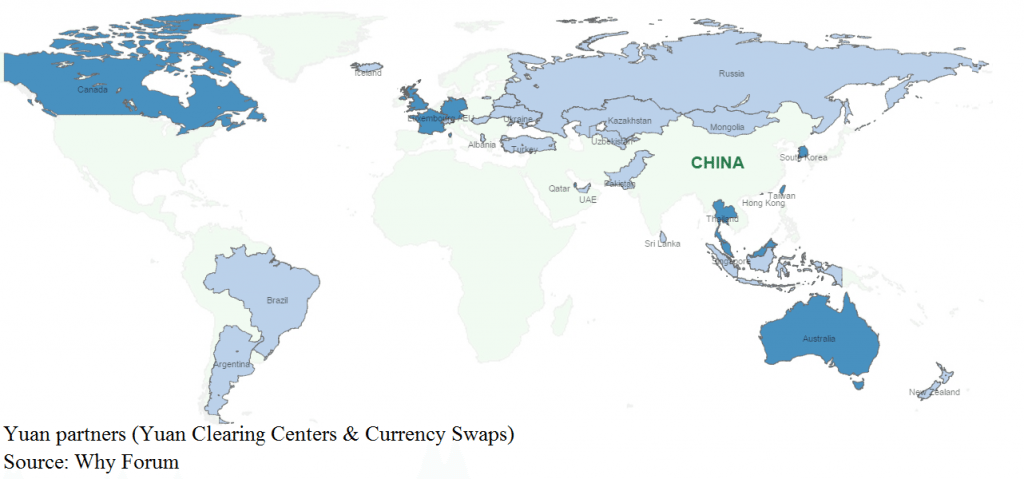

Yet, more structural motivations can be found. The credit lines from lender of last resort activity are part of the global development of the yuan.

While most all scholars agree that the dollar won’t be replaced any time soon, the global yuan infrastructure is nonetheless expanding. There are now 14 offshore clearing centers to convert local currency into yuan, and China has currency swaps agreements with 28 countries. Playing the role of lender of last resort for crisis countries has historically been a good way for a currency to acquire global influence.

The media also highlights the willingness to oppose the Western-led international financial order with the creation of institutions that compete with the World Bank and the IMF. This is the primary fear with the AIIB, the Silk Road Fund, and the BRICS development bank.

Much can be understood once we integrate the fact that Chinese lending started on a bilateral basis for years with a number of countries. From this perspective, the creation of multilateral institutions should be seen as a diversification away from bilateral relationships that have, indeed, become more and more risky.

Risky Friends

Chinese loans are increasingly risky business. as partners are all poorly rated, politically instable, and economically down. China is indeed facing credit risk from Venezuela (whose GDP is set to shrink by 7% this year), Zimbabwe, Ecuador and Argentina, all of which have repeatedly announced they won’t be able to repay the loans on time.

Moreover, the problem with Russia is not so much the probability of default as it is the political risk resulting from being alienated by the US. Relations with Ukraine, Myanmar, and Sri Lanka are also rife political risk, as the governments in the three countries have been replaced by leaders who are more suspicious about China. The move to multilateralism can, in this sense, be interpreted as China’s recognition of failure and a way to spread the risks.

Indeed, if Chinese motivations extend beyond short-term economic interests, Beijing should not be too concerned about potential losses. However, while China is known, contrary to the IMF, for attaching minimal conditions to its loans, the main focus should be on what conditions China will privately request from countries it saves.

Discussion

No comments yet.