By Jeffrey P. Snider, Alhambra Investment Partners

The Wall Street Journal reported a few days ago (h/t ZeroHedge) on the status of the ongoing disruption in domestic production of long haul trucks and vehicles. In what can only be confirmation of the state of US manufacturing, the huge drop in orders for new trucks matches shippers’ perceptions of the actual economic flow in goods. While economists want that to be an isolated circumstance of only manufacturing, goods activities account for a significant proportion of services as well. And it is getting bad:

The Wall Street Journal reported a few days ago (h/t ZeroHedge) on the status of the ongoing disruption in domestic production of long haul trucks and vehicles. In what can only be confirmation of the state of US manufacturing, the huge drop in orders for new trucks matches shippers’ perceptions of the actual economic flow in goods. While economists want that to be an isolated circumstance of only manufacturing, goods activities account for a significant proportion of services as well. And it is getting bad:

Orders for new big rigs plunged and inventories of unsold trucks soared to their highest levels since just before the financial crisis, as uncertainty about future demand and a weak market for freight transportation weighed on truck manufacturers.

About 67,000 Class 8 trucks are sitting unsold on dealer lots, after sales in March dropped 37% from a year earlier to 16,000 vehicles, according to ACT Research. Class 8 trucks are the type most commonly used on long-haul routes. Inventories haven’t been this high since early 2007, said Kenny Vieth, president of ACT.

It leaves no doubt that “something” is very wrong now in manufacturing and normal economic flow.

“Fleets are being very cautious in the current uncertain economic environment,” wrote Don Ake, a vice president with FTR Transportation Intelligence, which reported similar order numbers for March. “Freight has slowed due to the manufacturing recession, so they have sufficient trucks to meet current demand.”

Some of this reduction in 2016, as the Journal reports, is due to companies over-ordering in 2014 and 2015 based on the narrative that the economy was actually healing, or at worse would stay in its “new normal.” It raises the issue as to whether these conditions and the manufacturing recession they reflect are cyclical or structural; or both.

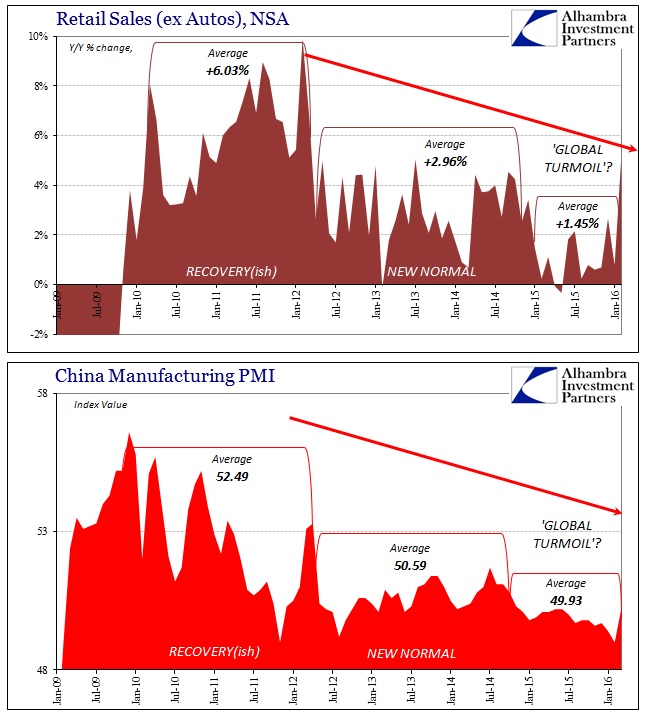

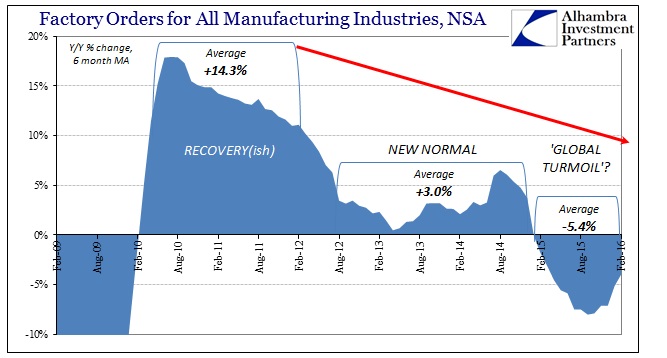

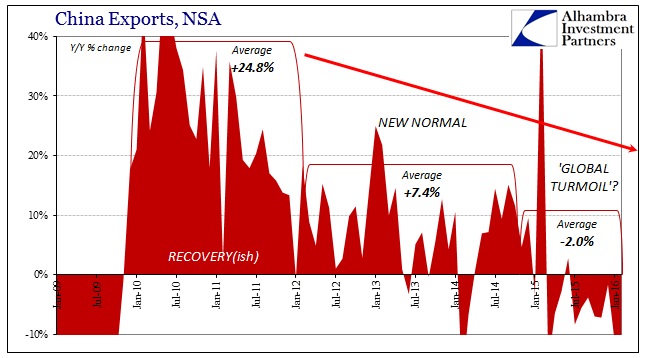

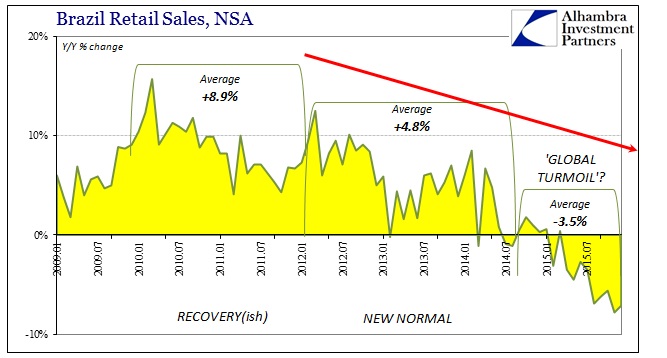

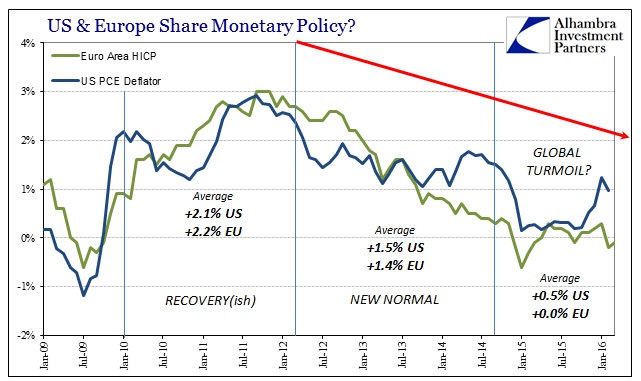

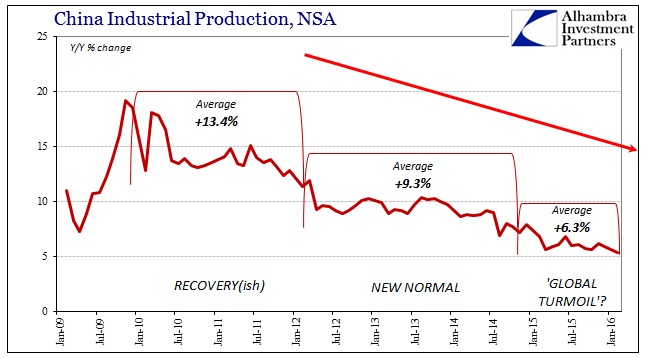

As I wrote yesterday, the contraction in goods and the US economy’s basis for them may or may not be heading toward recession. It is clear, however, that whatever the ultimate cycle reality there are deeper imbalances that run back several years, likely traced to decades of financialization that is now overturning, and thus really supersedes cyclical discussion. What we see in the US is not limited to the US, however; it is a global phenomenon, which can only mean one possible explanation.

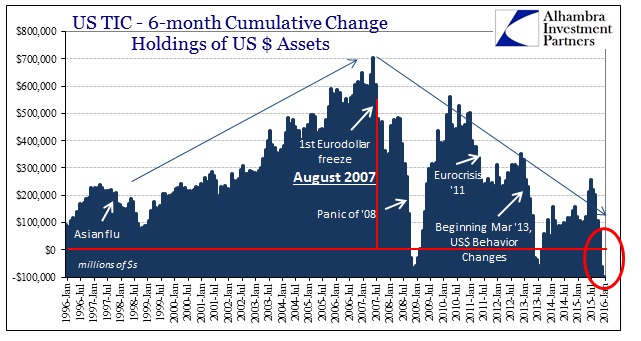

It is textbook economics (the real, common sense version, not orthodox econometrics). You have commodity prices falling and crashing, and then being met by puzzling restrictions in economic growth – a general and global slowdown dating back years. Because it doesn’t conform to the usual business cycle and because the monetary phenomenon we are talking about here isn’t consider “money” by economists, they ignore the obvious. This displays all the symptoms of shrinking money supply, and it all dates back to 2011.

It is, by far, much worse than just a recession, not the least of which is due to the distinct possibility that they could combine. More than that, since these are unique circumstances unlike anything observed in modern economic history we can’t really anticipate how or even where it might end and turn around. In many places, this money supply-driven slowdown has already achieved truly drastic proportions – and it only looks to continue.

Discussion

No comments yet.