By Mark Mobius, Templeton Emerging Markets Group

Pakistan is an example of a country many investors have shunned due to negative news and perceptions, but our take is that often things aren’t always as sensational as may be reported. We do know that we have found some well-run companies in which to invest. We also believe that Pakistan will attract wider investor interest in the coming years for a number of reasons.

Pakistan is an example of a country many investors have shunned due to negative news and perceptions, but our take is that often things aren’t always as sensational as may be reported. We do know that we have found some well-run companies in which to invest. We also believe that Pakistan will attract wider investor interest in the coming years for a number of reasons.

While Pakistan is currently classified as a frontier market, index provider MSCI announced in June that it would consider adding the MSCI Pakistan Index to the review list for its potential reclassification to emerging market status as part of the 2016 Annual Market Classification Review.1We approach investing on a stock-by-stock basis, so in terms of our investment process, we don’t really pay too much attention to these sorts of index changes. However, in the eyes of global investors, this potential change could bring heightened attention to Pakistan, along with greater international asset flows. Moreover, the consideration of the status upgrade reaffirms the ongoing efforts by the government and the potential we see in the country.

We have been investing in Pakistan for a number of years, and see it as an overlooked investment destination with attractive valuations due to negative macro sentiment. Pakistan has benefited from an improving growth outlook, continued efforts toward fiscal consolidation, steady progress in achieving structural reforms under the International Monetary Fund (IMF) program and ongoing support from regional partners.

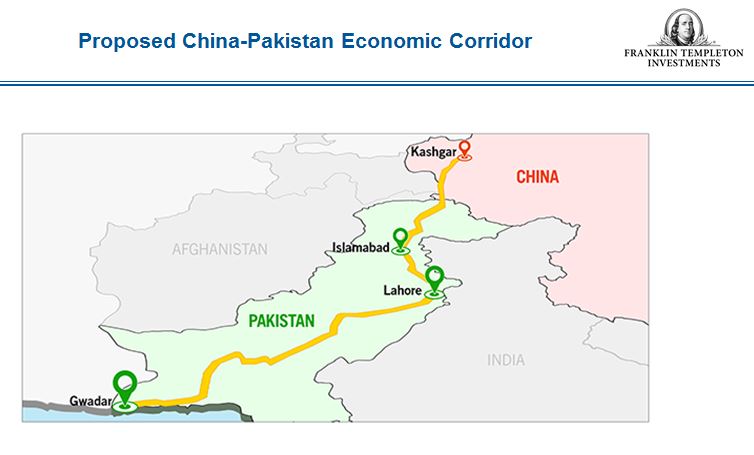

China-Pakistan Cooperation

China and Pakistan recently signed trade, energy and infrastructure agreements worth US$28 billion as part of a US$46 billion plan toward establishing the China-Pakistan Economic Corridor (CPEC), a combination of cooperative initiatives and projects that include connectivity, information network infrastructure, energy, industries and industrial parks, agricultural development and poverty alleviation, tourism and financial cooperation.2 Infrastructure projects associated with the CPEC, including the development of a deep-sea port offering direct access to the Indian Ocean and beyond, should help strengthen trade and investments in the region. China and Pakistan have a friendly partnership, and officials in China have dubbed the CPEC the flagship project of the broader “One Belt, One Road,” initiative, an ambitious plan to broaden China’s market connections to the rest of the world.

The announcement of these wide-ranging projects and the possibility of Pakistan’s move to emerging market status have stabilized the Pakistani economy and helped trigger gains in Pakistan’s stock market in recent years.

The Pakistani stock market has been one of the top-performing markets in the last five years (ended June 2015).3 The MSCI Pakistan Index has more than doubled with a 129% return during that time frame, compared with a 45% return for the MSCI Frontier Index and 22% increase in the MSCI Emerging Markets Index in US dollar terms.4 In our view, despite that strong performance, valuations of Pakistani stocks still remain relatively attractive. As of end-June 2015, the trailing price-to-earnings ratio of the MSCI Pakistan Index was 10 times, versus 11 times for the MSCI Frontier Index and 14 times for the MSCI Emerging Markets Index.5

Improving Fundamentals—and Fighting Terrorism

The country’s macroeconomic environment has been improving in recent years. In recent months, easing inflation has allowed Pakistan’s central bank to cut its benchmark interest rate to its lowest level in 42 years. The IMF currently forecasts gross domestic product growth in Pakistan of 4.3% this year and 4.7% in 2016, up from 2.6% in 2010.6 The fiscal situation has also been improving, supported by multilateral disbursements in recent years as well as a recent international Sukuk issuance.7 More recently, lower oil prices have also improved the country’s trade balance, although exports have been impacted by lower cotton prices and a stronger rupee.

Elsewhere, we believe government efforts on expenditure control and divestments have been positive, but the government will need to remain committed to the economic and structural reform program. For foreign investors, the most important concerns are security and political stability. An internal anti-terrorism drive was made in the wake of the tragic Peshawar incident in December 2014, which targeted schoolchildren. We think these efforts need to be maintained over the longer term to develop a better security climate for businesses and the society as a whole. In the political environment, delays in the implementation of reforms or deterioration in the political or security situation could adversely impact the country’s macroeconomic development and fiscal position, hinder investment and weaken investor confidence.

From a business perspective, the energy situation is another area of concern and also opportunity. Energy sector reforms need to be accelerated, including capital investments in every aspect of electric power: generation, distribution and transmission. Electricity tariff revisions and reduced electricity subsidies appear positive. Of course, those reforms can be more easily implemented now that prices of oil and gas have been coming down. We think it’s an ideal time for Pakistan to implement reforms that will put electric power supply on a sound financial footing, enabling adequate supply at a reasonable price for local businesses that need to be internationally competitive.

Despite a number of ongoing challenges, we see many reasons for a brighter future for Pakistan.

Mark Mobius’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

1. Source: MSCI, “Result of MSCI 2015 Reclassification Review,” June 9, 2015.

2. Source: Ministry of Planning, Development and Reform, Government of Pakistan.

3. Source: MSCI. Indexes are unmanaged, and one cannot directly invest in an index. Past performance does not guarantee future results. See www.franklintempletondatasources.com for additional data provider information.

5. The price-to-earnings ratio is the current market price of a company share divided by the earnings per share of the company.

6. Source: IMF World Economic Outlook database, April 2015. There is no assurance that any forecast will be realized.

7. Sukuk are Islamic financial certificates similar to bonds in Western financial markets that comply with Islamic religious law (Sharia).

Reblogged this on World Peace Forum.

LikeLike

Posted by daveyone1 | August 27, 2015, 9:11 pm