By Jeffrey P. Snider, Alhambra Investment Partners

If there is any doubt as to the confusion inside the FOMC, one needs only to examine its models. The latest updated projections make a full mockery of both monetary policy and the theory that guides it. Ferbus and the rest don’t buy the labor market story, either, which is why the Fed can only be hesitant at best about “normalization.” Coming from the (neo or not) Keynesian persuasion, what is showing up should never happen.

If there is any doubt as to the confusion inside the FOMC, one needs only to examine its models. The latest updated projections make a full mockery of both monetary policy and the theory that guides it. Ferbus and the rest don’t buy the labor market story, either, which is why the Fed can only be hesitant at best about “normalization.” Coming from the (neo or not) Keynesian persuasion, what is showing up should never happen.

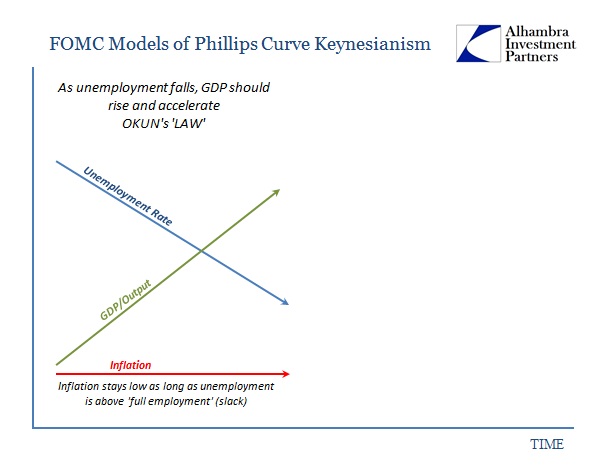

The theoretical notion of recovery is very straightforward in orthodox economics. In recession, the economy starts with high unemployment and therefore low inflation. Using the Phillips Curve as a short-term guide, orthodox models assume that as levels of unemployment begin to normalize, output (GDP) will rise. That will occur first without any uptick in inflation as the “slack” produced by the recession keeps price pressures to a minimum.

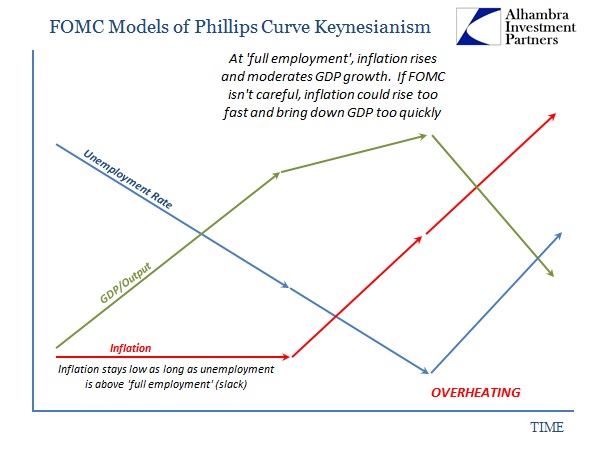

In Stage 1 everything is easy, so long as you can gain forward momentum in unemployment or output (which is what the QE’s were supposed to accomplish with regard to theoretical notions of hysteresis). Stage 2 gets slightly more complicated as the economy nears or reaches “full employment.” At that point, inflation should start to rise which will moderate output growth. If it progresses too far, that means the economy has reached “overheating” whereby inflation gets out of control and actively suppresses output, even reversing employment gains.

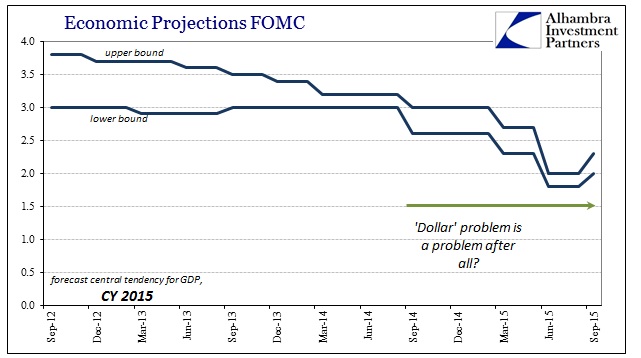

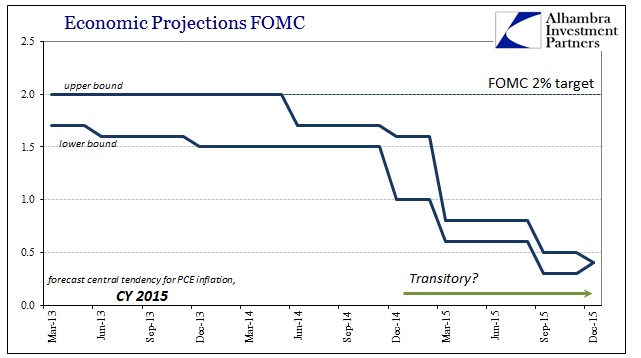

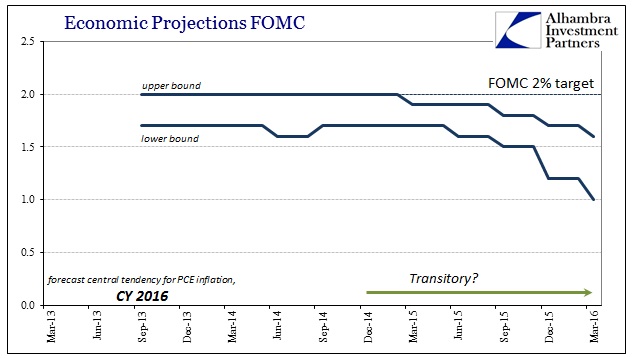

By the simple act of communicating a rate hike in December (though not actually carrying it out in meaningful fashion), the FOMC proclaimed closeness to overheating. But there is a huge problem with not just observed conditions but also projected economic conditions for the immediate future. If the economy and recovery has progressed sufficiently through Stage 2 to demand policy action before overheating, we should see a concurrent rise in inflation as well as output. The FOMC estimates show no such thing; worse, they estimate the opposite for especially inflation, as modeled GDP projections continue to muddle. That was true for not just CY 2015 as it was completed in full disappointment, but now encompassing CY 2016 as well.

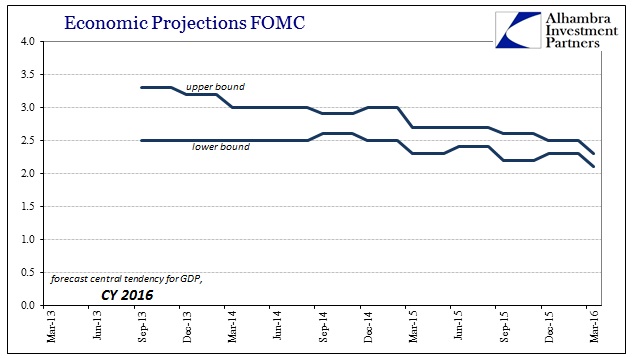

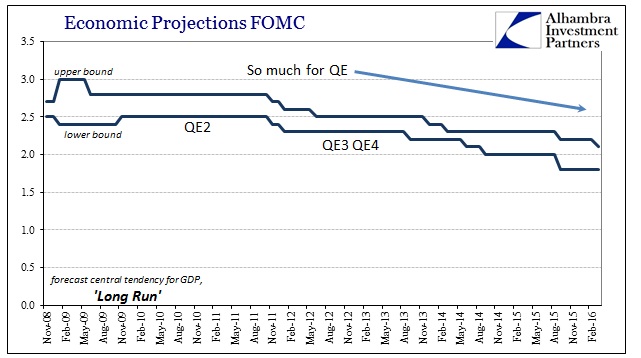

Both years start out in the earliest projections as they should according to theory, or close enough to be plausible; GDP should accelerate to at least something significantly better than the deficient output expansion of the recent past. Instead, as time rolls forward, that acceleration never materializes as GDP has stagnated around 2% year after year. The March 2016 projections show yet again another year absent acceleration in output (losing track of how many years in a row that would make).

In terms of inflation, the trends are even worse. When oil prices first crashed in late 2014/early 2015 that was demanded to be “transitory” uniformly across both models and orthodox interpretations (redundant, I know). A year later, not only did inflation never materialize for the rest of 2015, it is now modeled to be increasingly absent in 2016, as well.

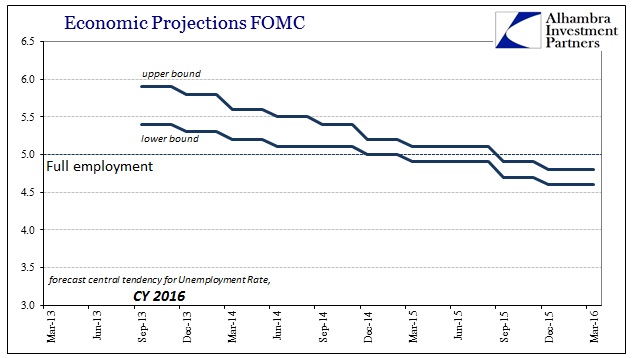

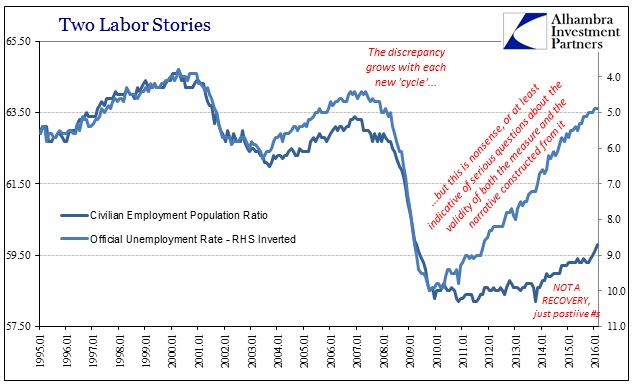

That’s a huge problem because the unemployment rate only gets better and better at each forecast. Back in late 2013 as the sounds of taper grew louder, the FOMC’s staff models projected the unemployment rate in 2016 would only be 5.4% to 5.9% (central tendency). That was forecast as a relatively slow improvement because output growth had been so lacking to that point, and even though it was expected to accelerate it was never thought to attain true recovery mechanics (something more like 4-5% rather than 3-3.5%). Instead, as noted above, GDP growth never accelerated at all – but the unemployment rate fell far faster than orthodox theory predicted anyway. In fact, so fast it asserts a major problem somewhere because Okun’s Law suggests GDP should have been, given the unemployment rate improvement, not just higher than 2.1% to 2.3% but higher than even the 3.3% once thought the upper bound back in 2013.

In other words, in late 2013 the models suggested relatively modest GDP of 2.5% to 3.3% in 2016 which would bring unemployment down also modestly to 5.4% and perhaps as high as 5.9%. That progress was supposed to be closing in on full employment enough to propel inflation very close to the 2% target for the PCE deflator. Instead, as of the March 2016 projections, the unemployment rate is expected to be enormously lower at just 4.6% to 4.8%, but GDP still stuck (and being downgraded each quarter) at 2.1% to 2.3% while inflation at the lower bound of the central tendency is 1%? One of these factors really doesn’t add up even in this orthodox context.

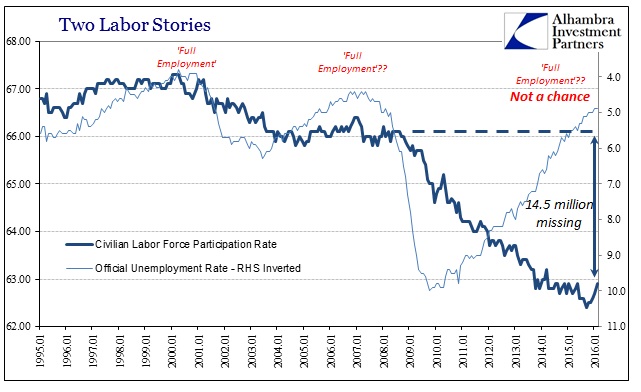

It isn’t difficult to determine which one, as persistently low calculated “inflation” is fully consistent with insufficient economic growth (or worse) for the nth year in a row. It is the huge and unexpected improvement in the unemployment rate blowing right on past “full employment” almost two years faster than predicted that is completely out of line; this “best jobs market in decades” that doesn’t project beyond really questionable BLS statistics.

As if to emphasize this statistical struggle against orthodox theory, the models are “forced” by the inequity between reported unemployment and the continuing disagreement via output and inflation to reduce to the long run growth rate estimate in order to make 2.2% growth seem like it could possibly belong in Stage 2 as if it were acceleration.

That means the unemployment rate is so far out of whack that the FOMC, a committee dedicated to believing in it above all else, really cannot base monetary policy on the most basic Keynesian, Phillips Curve assumptions. In fact, by count of even orthodox theory, the unemployment rate cannot be real. It doesn’t take much survey outside of these three variables to confirm the suspicion. As much as policymakers want it to be meaningful and representative, the fact that their own models not only fail to confirm it but openly refute it (with emphasis) is why Janet Yellen is slow on the rate hikes even though she talks about the jobs market at every opportunity (as if the unemployment rate as merely a number were, rational expectations, itself a stimulant that QE never was or could be).

It was the best jobs market in decades that once again finds nobody actually in it; not even the economists.

Discussion

No comments yet.